Many businesses receive funding shortly after approval

Built to help businesses explore realistic financing options

Business owners trust EquipFlow to simplify financing decisions

National and specialty lenders across industries

Your fastest route to the right lender — and the equipment your business needs.

Share your equipment type, business info, and location — it takes less than 60 seconds.

We instantly compare national and specialty lenders to find your best funding options.

Review offers, choose your lender, and get approved with fast turnaround times.

3D printer calculator searches online return hundreds of results—but they're all calculating the wrong thing. Every top result shows you what to charge customers per print job, not what it actually costs to buy, finance, and own the machine itself. Here's what nobody's telling you: a $777 desktop printer that seems affordable upfront carries $2,000-$15,000 in hidden costs over three years—filament waste from a 5% failure rate, energy bills from machines pulling 200-400 watts for hundreds of hours, and LCD screen replacements costing $200-$500 every few years.

What's worse? Most operators paying cash are leaving serious money on the table. According to IRS Publication 946, Section 179 allows businesses to deduct up to $2,560,000 in equipment purchases immediately. That $777 printer generates $194-$272 in first-year tax savings alone depending on your bracket—money you forfeit by waiting to save up cash. When you factor in 100% bonus depreciation and the opportunity cost of tied-up capital, financing becomes mathematically smarter for most businesses.

This calculator shows you the numbers everyone else ignores: total cost of ownership including materials, energy, labor, and failure waste, plus the real comparison between cash purchase and financing when tax benefits are properly calculated. Because the decision isn't whether you can afford a 3D printer—it's whether you can afford to make this decision without running the actual math.

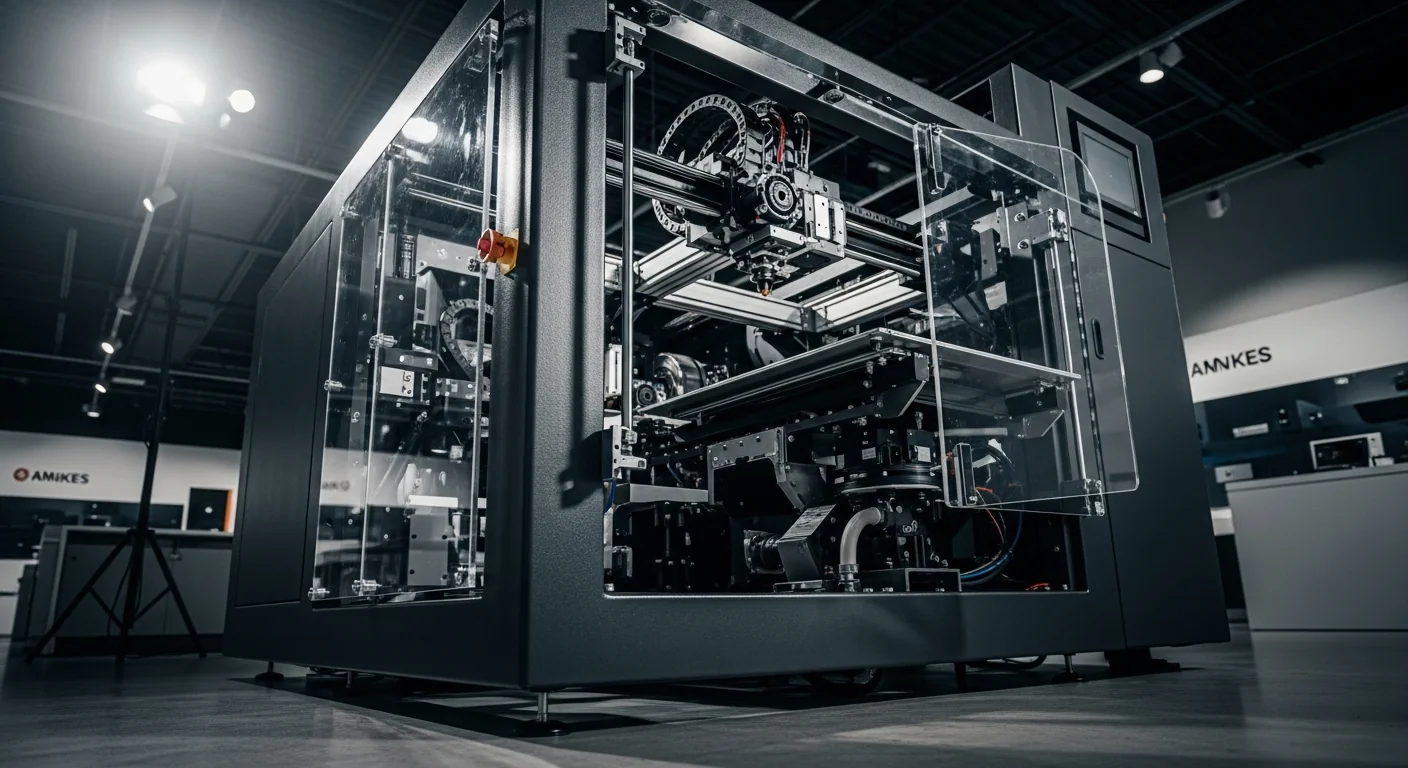

Here's the reality: buying a 3D printer is like buying a car—the sticker price is just the beginning. Desktop models range from $90 to $1,300 on major retailers, with professional units like the Bambu Lab H2C at $2,399 and industrial setups reaching $50,000+. But how much does a 3d printer really cost? The real cost story unfolds over 3,000-10,000 print hours of operation.

Consumer-grade desktop printers start around $90 for basic models and top out around $1,300 for feature-rich units. Professional prosumer models occupy the sweet spot—Bambu Lab's A1 Mini at $219, P1S at $399, and their top-tier H2C at $2,399. Industrial units serving production environments start around $5,000 and can exceed $50,000 for multi-material, large-format systems.

Material costs hit harder than most expect. PLA filament runs $15-25 per kilogram, with specialty materials costing 3-5x more. A standard spool contains about 1,080 feet of filament costing roughly $0.019 per foot. Factor in a 5% failure rate—one failed print in every 20—and material waste adds up quickly.

Energy consumption varies dramatically by printer type. Desktop units pull 100-150 watts, while enclosed heated printers consume 200-400 watts. Run a 300-watt printer 8 hours daily at $0.12/kWh, and you're looking at $105 annually just in electricity.

Labor time is the hidden killer. Setup takes 6-12 minutes per print, slicer customization adds 15-60 minutes, and nozzle changes consume 15-30 minutes. At a conservative $20/hour rate, labor costs often exceed material costs. A simple 3DBenchy that costs $0.51 in materials jumps to $3.51 when you factor in labor.

Most printers deliver 3,000-10,000 print hours before major component failures. Resin LCD screens last 2-3 years with replacement costs of $200-500. This creates a depreciation rate of 16.67-20% annually, with well-maintained 5-year-old equipment retaining only 50-60% of original value—if you can find buyers for outdated technology.

Smart operators understand that financing preserves working capital for revenue-generating activities. Before committing, explore 3d printer financing options for your setup. Current equipment financing rates break down by credit tier: A-tier borrowers (720+ credit) see 6-10% APR, B-tier (650-719) ranges 10-14%, and startups or thin-file businesses pay 12-18%.

Equipment Financing Agreements (EFAs) provide the cleanest structure—you own the equipment from day one, build equity, and qualify for full tax benefits. Fair Market Value leases offer lower monthly payments but leave you with no equity and potential end-of-lease charges. $1 buyout leases split the difference but often carry higher rates.

For professional setups, SBA Microloans provide up to $50,000—perfectly sized for a complete 3D printing operation including equipment, materials, and initial operating costs. The $50,000 limit aligns almost perfectly with a high-end professional setup: $2,399 for a Bambu Lab H2C, plus $5,000 in materials inventory, $10,000 for post-processing equipment, and $20,000+ for related tooling and software.

Documentation fees, automatic renewal clauses, and inflated end-of-lease purchase options destroy deals. We've seen lease-to-own programs where the total payments exceed 300% of the equipment's retail price. Personal guarantee requirements can put your house at risk for a $2,000 printer purchase—completely disproportionate to the actual risk.

Conventional wisdom says avoid debt for "nice-to-have" equipment. But when you run the actual numbers, financing often wins. To better understand your options, compare the best 3d printer options available before deciding. Here's why: Section 179 allows businesses to deduct the full purchase price of qualifying equipment up to $2,560,000 in the year it's placed in service. Bonus depreciation adds another 20% first-year deduction on remaining basis.

For larger investments, the numbers become compelling. A $50,000 professional setup generates approximately $10,500 in first-year tax savings at the 21% corporate rate, effectively reducing your net equipment cost to $39,500 while preserving your working capital through financing.

At a 40% profit margin—standard pricing for most 3D printing services—a financed $777 printer needs to generate $1,295 in gross revenue to break even after financing costs and tax benefits. Factor in the 5% failure rate and actual operating costs, and you're looking at roughly 450-500 successful prints to payoff.

For businesses already generating 15-20% annual ROI on working capital, financing becomes a no-brainer. The opportunity cost of tying up $50,000 cash ($7,500-$10,000 annually) exceeds the financing cost at current rates.

Equipment financing approval depends more on business cash flow than personal credit for established businesses. A-tier approval (700+ credit, 2+ years in business) opens all doors with minimal documentation—often just a 2-page application for deals under $150,000.

B-tier borrowers need more documentation: 3 months of bank statements, basic P&L, and sometimes personal financials. Startups face the biggest hurdles but have options: SBA Microloans through nonprofit lenders, or equipment-secured financing where the printer itself serves as collateral.

Time-in-business requirements vary by lender. Traditional banks want 2+ years of operating history. Alternative lenders work with businesses as young as 6 months. Startups often need personal guarantees, but these should be limited to the equipment value—never unlimited personal liability.

The 3D printing market is exploding—from $29.29 billion in 2025 to a projected $134.58 billion by 2034, representing 19% compound annual growth. This rapid expansion brings both opportunity and risk.

Technology obsolescence accelerates in fast-growing markets. Features that were premium options 18 months ago—auto-bed leveling, multi-color printing, enclosed chambers—are now standard on sub-$500 units. This argues for shorter financing terms that preserve upgrade flexibility rather than 5-7 year leases that lock you into outdated technology.

AI integration and automated workflow optimization are becoming standard. 4D printing—programmable materials that change shape after printing—will grow from $650 million in 2025 to $4.1 billion by 2030. Financing terms should align with technology refresh cycles, not just equipment lifespan.

OSHA workplace safety standards apply to 3D printing operations, particularly regarding ventilation for fume extraction and burn protection around nozzles reaching 320°C. Recent regulatory updates show OSHA penalties ranging from $1,190-$16,550 for serious violations, with willful violations carrying penalties of $11,524-$165,514.

Put that in perspective: a single willful OSHA violation penalty could buy 125+ desktop printers or fund multiple complete professional setups. This makes safety compliance a capital preservation strategy, not just regulatory compliance. Budget $500-$2,000 for proper enclosure and ventilation in your total cost of ownership calculations.

We've seen too many businesses get trapped in expensive lease-to-own programs or personal guarantees that put their house on the line. Here's how we help you avoid those traps and find legitimate equipment financing:

Ava analyzes your specific situation—whether you're buying a $219 desktop printer or a $50,000 industrial setup. She factors in your business financials, time in operation, and credit profile to determine which lenders will actually compete for your deal. No point applying to lenders who automatically reject startups or equipment over certain age limits.

Instead of you calling 12 different lenders and getting rejected by half of them, Ava matches you with 3-4 lenders in our network who specialize in your equipment type and credit tier. When lenders compete for the same deal, rates typically drop 0.5-2 percentage points. That's real money—on a $50,000 printer, 1.5% rate reduction saves you $4,200 over a 5-year term.

You'll see exactly how each offer affects your monthly cash flow, total cost, and tax position. No hidden fees, no surprise end-of-term charges, no automatic renewal clauses. Everything's laid out so you can make the decision based on math, not sales pressure.

You maintain complete control. No obligation to accept any offer, no impact on your credit for the initial match, no pressure tactics. Choose the offer that makes financial sense for your operation—or walk away if none do.

We've seen too many businesses get trapped in expensive lease-to-own programs or personal guarantees that put their house on the line. Here's how we help you avoid those traps and find legitimate equipment financing:

Ava analyzes your specific situation—whether you're buying a $219 desktop printer or a $50,000 industrial setup. She factors in your business financials, time in operation, and credit profile to determine which lenders will actually compete for your deal. No point applying to lenders who automatically reject startups or equipment over certain age limits.

Instead of you calling 12 different lenders and getting rejected by half of them, Ava matches you with 3-4 lenders in our network who specialize in your equipment type and credit tier. When lenders compete for the same deal, rates typically drop 0.5-2 percentage points. That's real money—on a $50,000 printer, 1.5% rate reduction saves you $4,200 over a 5-year term.

You'll see exactly how each offer affects your monthly cash flow, total cost, and tax position. No hidden fees, no surprise end-of-term charges, no automatic renewal clauses. Everything's laid out so you can make the decision based on math, not sales pressure.

You maintain complete control. No obligation to accept any offer, no impact on your credit for the initial match, no pressure tactics. Choose the offer that makes financial sense for your operation—or walk away if none do.

We've seen too many businesses get trapped in expensive lease-to-own programs or personal guarantees that put their house on the line. Here's how we help you avoid those traps and find legitimate equipment financing:

Ava analyzes your specific situation—whether you're buying a $219 desktop printer or a $50,000 industrial setup. She factors in your business financials, time in operation, and credit profile to determine which lenders will actually compete for your deal. No point applying to lenders who automatically reject startups or equipment over certain age limits.

Instead of you calling 12 different lenders and getting rejected by half of them, Ava matches you with 3-4 lenders in our network who specialize in your equipment type and credit tier. When lenders compete for the same deal, rates typically drop 0.5-2 percentage points. That's real money—on a $50,000 printer, 1.5% rate reduction saves you $4,200 over a 5-year term.

You'll see exactly how each offer affects your monthly cash flow, total cost, and tax position. No hidden fees, no surprise end-of-term charges, no automatic renewal clauses. Everything's laid out so you can make the decision based on math, not sales pressure.

You maintain complete control. No obligation to accept any offer, no impact on your credit for the initial match, no pressure tactics. Choose the offer that makes financial sense for your operation—or walk away if none do.

Most business owners call lenders randomly and get frustrated with rejections, inconsistent rate quotes, and pushy sales tactics. We've built a smarter system that puts you in control.

When 3-4 lenders compete for the same deal, rates typically drop 0.5-2 percentage points. On a $50,000 industrial printer, that 1.5% rate reduction saves you $4,200 over a 5-year term. Ava's matching algorithm identifies lenders who actually want your specific deal profile—no wasted time with lenders who automatically reject your industry or credit tier.

Generic equipment lenders often reject 3D printer financing because they don't understand the market or technology. Ava specializes in finding lenders who understand depreciation curves, technology refresh cycles, and the rapid market growth that actually supports equipment values. Banks that reject equipment over 7 years old won't be a problem for 3D printers that typically refresh every 2-3 years anyway.

Every day without the right equipment costs money. Production delays, missed deadlines, and rental expenses add up quickly. Ava can match you with competing lenders within 24 hours, with most approvals following within 48 hours. Compare that to calling lenders individually and waiting weeks for responses.

No impact on your credit score for the initial matching process. No obligation to accept any offer. No pushy sales tactics or bait-and-switch rate games. You get real offers from real lenders, make your decision based on math, and move forward only if the numbers work for your business.

Most business owners call lenders randomly and get frustrated with rejections, inconsistent rate quotes, and pushy sales tactics. We've built a smarter system that puts you in control.

When 3-4 lenders compete for the same deal, rates typically drop 0.5-2 percentage points. On a $50,000 industrial printer, that 1.5% rate reduction saves you $4,200 over a 5-year term. Ava's matching algorithm identifies lenders who actually want your specific deal profile—no wasted time with lenders who automatically reject your industry or credit tier.

Generic equipment lenders often reject 3D printer financing because they don't understand the market or technology. Ava specializes in finding lenders who understand depreciation curves, technology refresh cycles, and the rapid market growth that actually supports equipment values. Banks that reject equipment over 7 years old won't be a problem for 3D printers that typically refresh every 2-3 years anyway.

Every day without the right equipment costs money. Production delays, missed deadlines, and rental expenses add up quickly. Ava can match you with competing lenders within 24 hours, with most approvals following within 48 hours. Compare that to calling lenders individually and waiting weeks for responses.

No impact on your credit score for the initial matching process. No obligation to accept any offer. No pushy sales tactics or bait-and-switch rate games. You get real offers from real lenders, make your decision based on math, and move forward only if the numbers work for your business.

Most business owners call lenders randomly and get frustrated with rejections, inconsistent rate quotes, and pushy sales tactics. We've built a smarter system that puts you in control.

When 3-4 lenders compete for the same deal, rates typically drop 0.5-2 percentage points. On a $50,000 industrial printer, that 1.5% rate reduction saves you $4,200 over a 5-year term. Ava's matching algorithm identifies lenders who actually want your specific deal profile—no wasted time with lenders who automatically reject your industry or credit tier.

Generic equipment lenders often reject 3D printer financing because they don't understand the market or technology. Ava specializes in finding lenders who understand depreciation curves, technology refresh cycles, and the rapid market growth that actually supports equipment values. Banks that reject equipment over 7 years old won't be a problem for 3D printers that typically refresh every 2-3 years anyway.

Every day without the right equipment costs money. Production delays, missed deadlines, and rental expenses add up quickly. Ava can match you with competing lenders within 24 hours, with most approvals following within 48 hours. Compare that to calling lenders individually and waiting weeks for responses.

No impact on your credit score for the initial matching process. No obligation to accept any offer. No pushy sales tactics or bait-and-switch rate games. You get real offers from real lenders, make your decision based on math, and move forward only if the numbers work for your business.

Most business owners call lenders randomly and get frustrated with rejections, inconsistent rate quotes, and pushy sales tactics. We've built a smarter system that puts you in control.

When 3-4 lenders compete for the same deal, rates typically drop 0.5-2 percentage points. On a $50,000 industrial printer, that 1.5% rate reduction saves you $4,200 over a 5-year term. Ava's matching algorithm identifies lenders who actually want your specific deal profile—no wasted time with lenders who automatically reject your industry or credit tier.

Generic equipment lenders often reject 3D printer financing because they don't understand the market or technology. Ava specializes in finding lenders who understand depreciation curves, technology refresh cycles, and the rapid market growth that actually supports equipment values. Banks that reject equipment over 7 years old won't be a problem for 3D printers that typically refresh every 2-3 years anyway.

Every day without the right equipment costs money. Production delays, missed deadlines, and rental expenses add up quickly. Ava can match you with competing lenders within 24 hours, with most approvals following within 48 hours. Compare that to calling lenders individually and waiting weeks for responses.

No impact on your credit score for the initial matching process. No obligation to accept any offer. No pushy sales tactics or bait-and-switch rate games. You get real offers from real lenders, make your decision based on math, and move forward only if the numbers work for your business.

.png)